The $80 Billion Pivot: Decoding Alphabet's Capital Raise and the AI Ecosystem Squeeze

How Google's massive equity financing is reshaping hyperscale infrastructure, power grids, and the custom silicon market.

Alphabet’s ($GOOGL) recent $80 billion equity financing plan is a massive, structural pivot signaling that the capital requirements for the AI arms race have crossed a threshold where even a cash-printing machine cannot fund it entirely from internal operations and debt.

This isn’t just a funding round. It is a strategic maneuver that alters the trajectory of custom silicon designers and the physical power grid. Here is a breakdown of the capital pivot, the infrastructure reality driving it, and the ripple effects across the broader AI ecosystem.

The Capital Structure Pivot & Leverage Limits

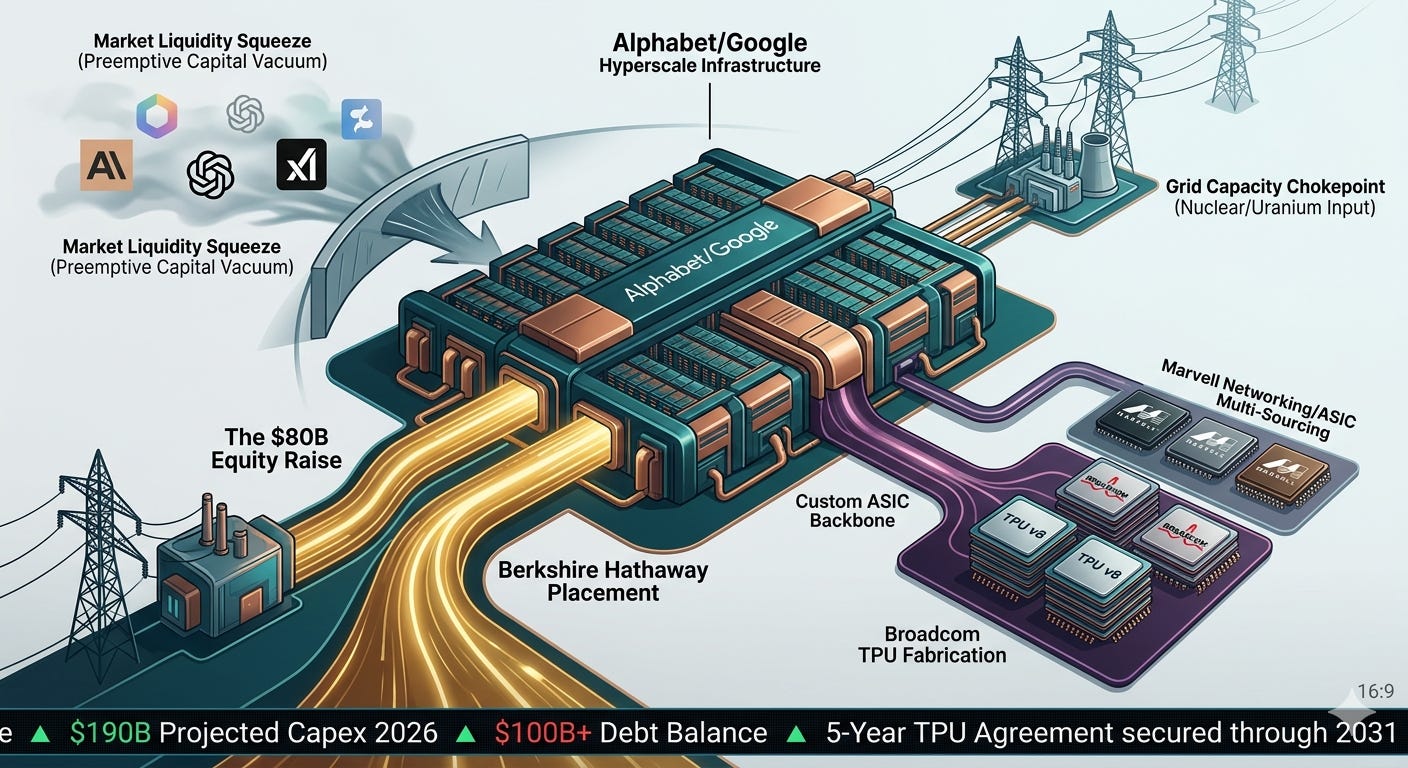

Alphabet currently generates north of $170 billion in operating cash flow over a trailing 12-month period, backed by massive cash reserves. However, the sheer burn rate required to maintain dominance is staggering. During their Q1 2026 earnings, Alphabet projected that capital expenditures will reach $180 billion to $190 billion by 2026.

Alphabet has traditionally relied on its cash flow and the bond market to fund growth. But having recently issued yen, GBP, and USD bonds, their total debt balance has pushed past the $100 billion mark. Relying solely on bonds at this stage chokes the balance sheet. Issuing equity is the necessary pressure release valve to sustain this historic capex avalanche.

The Berkshire Endorsement Crucially, this raise is anchored by a highly unusual $10 billion private placement to Berkshire Hathaway. Warren Buffett and Greg Abel acquiring $5 billion in Class A shares and $5 billion in Class C shares at a discount is a massive signal. Berkshire wants defensive, compounding assets. This placement allows them to take a commanding position in the infrastructure layer of the future without moving the open market price against themselves.

The Strategic Liquidity Squeeze

Beyond balance sheet management, there is a highly tactical, competitive edge to this raise.

By pulling $80 billion of liquidity out of the public equity markets comprising a $30 billion public offering and a $40 billion at-the-market (ATM) program starting in Q3 Alphabet is preemptively vacuuming up investor capital. Companies like Anthropic, OpenAI, and xAI are approaching the window where they need public offerings to fund their own infrastructure. Alphabet is effectively playing hardball, starving the impending IPO windows of its direct competitors.

The Grid Chokepoint: The Silicon-to-Glass S-Curve

The market initially treated the AI buildout as a pure silicon play. But the $80 billion isn’t just flowing to chip designers, it is being deployed into physical, industrial-scale infrastructure.

As we track the Silicon-to-Glass S-Curve, the primary bottleneck for AI expansion has shifted from securing GPUs to securing system capacity: energized sites, grid certainty, cooling infrastructure, and transformer availability. You cannot deploy tens of billions into hyperscale data centers without securing massive, uninterrupted base-load power.

This infrastructure reality is the exact catalyst aggressively repricing the nuclear sector and the uranium complex. The power grid is the new chokepoint for tech expansion.

The Silicon Derivative: $AVGO vs. $MRVL

For the semiconductor space, Alphabet’s raise is the direct funding mechanism for the custom ASIC backlog. When a hyperscaler secures this level of liquidity, it de-risks the out-year revenue projections for its primary design partners.

The 5-Year TPU Master Agreement: Broadcom ($AVGO) recently formalized a massive structural agreement via an 8-K filing a 5-year contract securing them as the designer and supplier for future TPU generations through 2031, including the TPU v8 variants (Sunfish and Zebrafish). Alphabet’s liquidity ensures the balance sheet capacity to execute these massive purchase orders, supporting Broadcom’s target of $100 billion in AI chip revenue by 2027.

The Anthropic Compute Backstop: This capital also injects liquidity into the broader ecosystem, supporting Broadcom’s active role in backstopping a complex financing structure to secure 3.5 gigawatts of TPU-based compute for Anthropic by 2027.

The Multi-Sourcing Threat However, a war chest this large also funds vendor diversification. Alphabet is actively multi-sourcing its custom silicon to prevent vendor lock-in. Marvell ($MRVL) has secured a portion of the next-generation TPU work, ending Broadcom’s perceived monopoly on the flagship program. While the overall capex pie is expanding massively, the fundamental dynamics of the $AVGO vs. $MRVL pair trade are shifting. Broadcom remains the incumbent heavyweight, but Marvell is now capturing critical incremental growth.

The Bottom Line

When a mega-cap tech giant moves $80 billion, the shockwaves reshape the landscape. The physical power grid and custom ASIC designers are the true, leveraged derivatives of this capital raise. Track the hyperscaler capex, but monitor the supplier allocations and the baseload power contracts.

This analysis was powered by the ARMR Method™. To get my real-time insights, full portfolio access, and join a community of serious investors, explore our premium services

DISCLAIMER: All of ARMR Report, our trades, strategies, and news coverage are based on our opinions alone and are only for entertainment purposes. You should not take any of this information as guidance for buying or selling any type of investment or security. I am only sharing my biased opinion based off of speculation and personal experience. An individual trader’s/investor’s results may not be typical and may vary from person to person. It is important to keep in mind that there are risks associated with investing in the stock market and that one can lose all of their investment. Thus, trades/investments should not be based on the opinions of others but by your own research and due diligence.