As Code Goes to Zero, Design Goes to Infinity: The Bull Case for Figma (NYSE: FIG)

Navigating the Software Reset and the Generational Entry Point for the Future of UI/UX

The Core Reality: We are entering an era where AI makes writing code cheaper and faster. As the barrier to building software plummets, the economic bottleneck violently shifts to designing and defining what to build. Figma sits precisely at this choke point.

Figma (NYSE: FIG) is no longer just a digital canvas; it is the operating system for digital product creation. Operating on a product-led growth (PLG) model, it monetizes via subscription tiers targeting designers, product managers, and software engineers. Figma acts as the single source of truth where design systems, front-end code components, and product strategy converge. They do not just draw the buttons—they orchestrate the workflow of the modern software enterprise.

Here is a deep dive into why the recent structural reset in Figma’s valuation presents a generational entry point.

📊 Fundamental Deep Dive & The Value Shift

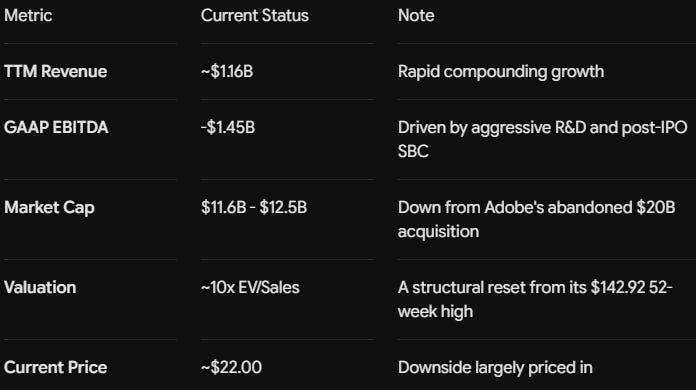

The macro environment has caused a broad software sector de-rating, but the underlying engine at Figma is compounding. The premium has washed out; the growth has not.

Key Financial Metrics

Capital Allocation & Insider Activity: Management is running a pure reinvestment playbook. Capital return (dividends/buybacks) is non-existent, which is appropriate for this growth stage. While recent regulatory filings indicate standard post-IPO insider selling (e.g., Brendan Mulligan, Tyler Herb), institutional accumulation is providing a sturdy floor.

The Value Shift: The secular shift is violently pro-Figma. Because GenAI tools compress development time, enterprises are initiating more software projects than ever before. Every new AI-assisted coding cycle requires a top-of-funnel design phase. Figma captures this volume spike perfectly.

🗺️ Strategic Roadmap & Quantifiable Tailwinds

Figma is actively expanding its footprint beyond the design department, targeting the entire product development lifecycle.

The Next 3 Years: Forward Roadmap

Dev Mode Monetization: Bridging the final gap between static design and live code, capturing lucrative engineering budgets alongside design budgets.

Native AI Generation: Embedding text-to-UI, automated asset tagging, and generative layout variations directly into the canvas.

Enterprise Collaboration (FigJam): Expanding laterally into whiteboarding and strategy, directly attacking the broader PM and marketing software stack.

Quantifying the Tailwind (The Enterprise ROI): A standard enterprise deployment involves a 10:1 ratio of developers to designers. In legacy workflows, design hand-off friction wastes roughly 15% of a front-end developer’s week. By centralizing the design system in Figma, a 100-person engineering org (at a $150k average salary) recovers over $2.25M in wasted productivity annually. The software pays for its enterprise license within the first 60 days.

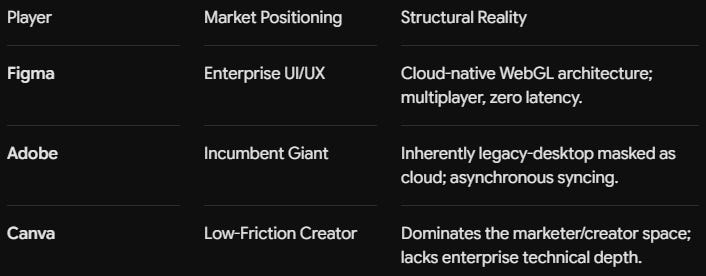

🏰 Competitive Ecosystem & The Moat

Figma stands alone in the highly technical, professional enterprise UI/UX arena. Adobe failed to buy them; they cannot out-build them.

The Titans Compared

Moat Analysis

Network Effects: Designers build plugins, templates, and public assets in the Figma Community, drawing in a continuously growing user base.

Absolute Switching Costs: Once a Fortune 500 company builds its proprietary “Design System” (component libraries, brand rules, interactive states) inside Figma, ripping it out requires halting the entire software production line. The lock-in is near-absolute.

⚠️ Catalyst Watch & Risk Profile

The Bull Case (Upside Drivers)

Accelerated enterprise adoption of Dev Mode seats.

A faster-than-expected macro pivot leading to a resurgence in enterprise IT/software spending.

Successful upselling of premium AI features to the existing user base.

The Bear Case (Downside Risks)

A protracted “software apocalypse” forcing tech companies to freeze headcount, thereby capping Figma’s seat-based revenue growth.

Emerging threats from AI foundational models attempting to bypass wireframing entirely via “prompt-to-app” generation.

Catalysts to Watch

Hard Catalyst: The next earnings print on September 2, 2026. Forward guidance will dictate if the current valuation floor holds.

Soft Catalyst: The annual Config conference. Any announcements regarding next-gen autonomous design features will force immediate re-ratings by tech analysts.

🎯 Synthesis & The Bottom Line

The 2026 software reset has provided a generational entry point for an undisputed category leader. Trading at ~10x sales for a company driving the core infrastructure of digital product creation presents a highly asymmetric risk/reward profile. The downside is largely priced into the $22 stock; the upside leverages the entirety of the AI software boom.

Strategic Signal: High Conviction Buy

AI does not replace Figma; it supercharges its utility. As the cost of code goes to zero, the value of design goes to infinity. Figma is the tollbooth for the next decade of software development.

This analysis was powered by the ARMR Method™. To get my real-time insights, full portfolio access, and join a community of serious investors, explore our premium services

DISCLAIMER: All of ARMR Report, our trades, strategies, and news coverage are based on our opinions alone and are only for entertainment purposes. You should not take any of this information as guidance for buying or selling any type of investment or security. I am only sharing my biased opinion based off of speculation and personal experience. An individual trader’s/investor’s results may not be typical and may vary from person to person. It is important to keep in mind that there are risks associated with investing in the stock market and that one can lose all of their investment. Thus, trades/investments should not be based on the opinions of others but by your own research and due diligence.